What is the Law of Supply and Demand in Economics?

Reading time: 6 minutes

When learning about or working with market systems, you will likely hear the concepts of supply and demand.

These are foundational economic concepts for the market economy in which most of the world operates and how prices in almost all things are determined. Here, we review the basic microeconomic concepts of supply and demand and how this economic theory affects prices in free market economies.

Demand

Demand is one of the fundamental laws of our economic systems. It describes the relationship between the price, quantity, willingness, and ability of consumers to purchase a good or service.

In its most basic form, the law of demand states that there is an inverse relationship between the price of a good and the quantity demanded, ceteris paribus (or all else being equal).

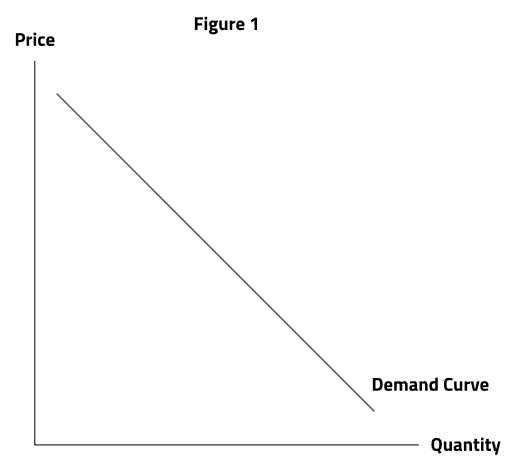

Economists like to graph this relationship with what is known as a ‘demand curve’, shown in Figure 1, with quantity represented on the horizontal axis and price on the vertical axis.

As seen in the downward slope of the graph, when the price increases, the quantity demanded decreases, whereas, at lower prices, the quantity demanded is higher. There are a few reasons for this inverse relationship, including the substitution effect, the income effect, and the law of diminishing marginal utility.

The substitution effect refers to the ability of a given good to be substituted for another good. Take the example of apples and oranges. If the price of apples increases and the price of oranges is lower, consumers are more likely to substitute apples for oranges as they are similar fruits, but one has a lower cost. The strength of the substitution effect depends on the number and similarity of substitute products.

The income effect refers to the change in quantity demanded depending on the purchasing power of consumers. If consumer incomes are high, the quantity demanded of a good will be higher, as the relative cost to consumers for purchasing that good is lower and vice versa.

The law of diminishing marginal utility refers to the lowered marginal utility we get for each unit of a good we consume. For example, if a consumer purchases a vacuum cleaner, it gives them the ability to clean things faster than if they had to do it by hand, and therefore, they might be willing to pay a higher price. However, a second vacuum cleaner will add much less utility to their lives, and so the price would need to be much lower for it to be worth that small amount of marginal utility.

Supply

The law of supply is the microeconomic concept that describes the fundamental economic relationship between price, quantity willingness, and ability of suppliers to provide a good or service in the market.

The law of supply states that ceteris paribus (all else being equal), as a good or service’s price rises, so too does the quantity supplied, and as the price falls, so too does the quantity supplied.

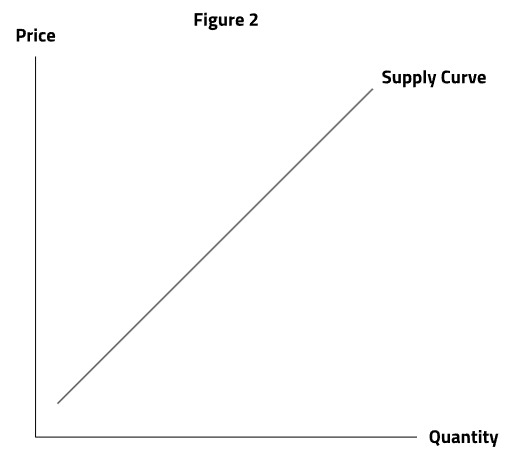

Economists usually illustrate this relationship with what is known as a ‘supply curve’, as shown in Figure 2, with quantity being represented on the horizontal axis and price on the vertical axis.

As seen in the upward slope of the curve, at high prices, the quantity supplied is high, and at lower prices, the quantity supplied decreases. There are a few reasons for this relationship, including the profit motive for suppliers, new market entrants, the cost of production, and opportunity cost.

The profit motive is usually the main driver for the force of supply. As the price of the product increases, it becomes more profitable and therefore, suppliers will be motivated to produce more, increasing the quantity supplied. The increased profit motive can also cause new entrants to be motivated to enter the market, meaning there are more producers of a given product, and as a result, the quantity of goods supplied also increases.

Production costs also explain this relationship, as increasing production usually involves costs that could come from paying overtime for labour or buying more machinery or similar capital to increase production. This means that to increase production, the price needs to increase to fund this expansion.

Opportunity cost (meaning the cost of giving up the next best alternative) is also a determining factor in the behaviour of the supply curve. This is because producers have the option to produce other goods, and so producers are more likely to shift resources to goods that increase in price to increase their profits.

Supply and Demand

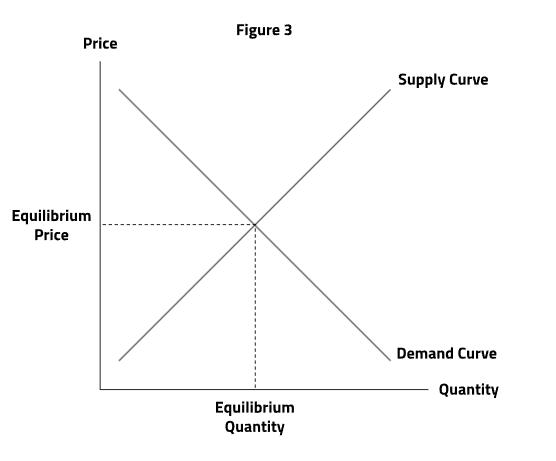

We now understand how supply and demand behave according to price, but what determines price? In a free and competitive market, the price of a product is determined by the intersection of supply and demand curves where the quantity supplied and quantity demanded are equal. This is illustrated in Figure 3, shown below, with the price of the intersection known as the ‘equilibrium price’ or the ‘market clearing price’ and the quantity known as the ‘equilibrium quantity’.

The price and quantity will always move towards the market equilibrium point because if the price is too high, this will create a surplus. This excess supply should signal producers that they need to lower their prices to clear out their excess stock. Conversely, if the price is lower than the equilibrium price, there will be a shortage, signalling to producers that they should increase their prices as they can make a greater profit.

Keep in mind that supply and demand are not stationary, which causes fluctuations in the prices of goods or services. These demand increases and decreases, as well as supply movements, are known to economists as supply and demand shifts and usually cause surpluses or shortages in the short term, as price corrects.

Things that affect demand include changes in consumer income, the price of related goods, changes in consumer preferences, consumer confidence, the availability and terms of credit, new information or shocks such as geopolitical events or natural disasters. Things that cause supply increases or decreases include changes in the costs of inputs (such as cheaper materials or labour), changes in technology, taxes or subsidies, access to credit, market competition, regulations, and external shocks.

Conclusion

This article serves as a basic explanation of the economic principles of supply and demand and how they are constantly interacting to determine the market price of the goods in our economies. There are some exceptions to these laws, but in most scenarios, particularly in competitive markets, these laws apply.